AMD Stock at $168 Surges After Q2 Beats; MI350 Ramp and $1 B Free Cash Flow Spark Upside

With gross margins steady at 54% and record EPYC CPU sales, Advanced Micro Devices stock eyes mid-$200s on inference-led demand and China catalyst | That's TradingNEWS

Resilient Q2 Performance Fuels Confidence In NASDAQ:AMD’s Growth Trajectory

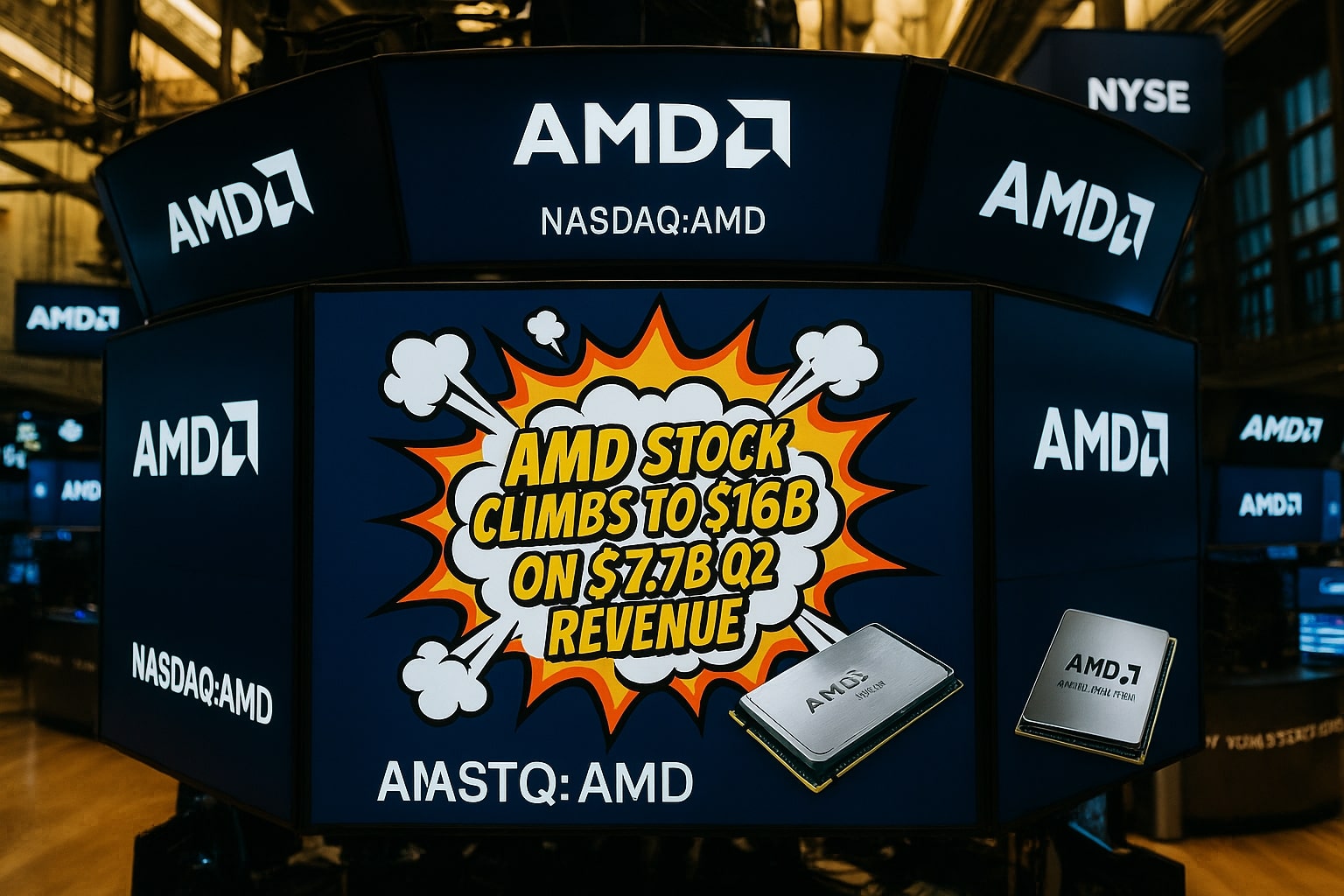

Advanced Micro Devices surpassed consensus with $7.7 billion in second-quarter revenue, marking a 23 percent year-over-year increase despite the absence of China sales in guidance. Non-GAAP gross margin held steady at 54 percent, even after absorbing an $800 million inventory write-down tied to export controls. Free cash flow surged past $1 billion, driven by a rebound in consumer and gaming segments, where Ryzen desktop units and Radeon 9600 XT graphics cards powered a combined 73 percent quarterly jump to $1.1 billion. The surprising resilience of the client computing business—up 67 percent to $2.5 billion on record notebook and desktop CPU sales—underscores AMD’s ability to offset data-center headwinds and maintain robust cash generation as it diverts growth initiatives toward higher-margin opportunities.

MI350 Ramp And Sovereign AI Partnerships Anchor The Back Half Outlook

The phased introduction of the MI350 GPU in June laid the groundwork for a powerful second-half ramp. Performance benchmarks demonstrate parity or outperformance against Nvidia’s B200 architecture in inference workloads, delivering up to 40 percent more tokens per dollar at lower system complexity. High-profile cluster wins—including Oracle’s 27,000-node deployment integrating MI355X accelerators alongside fifth-generation EPYC CPUs—signal a pronounced shift toward AMD-powered inference infrastructure. More than forty sovereign AI engagements, including a $10 billion Saudi rollout over five years with HUMAIN, reinforce management’s conviction that inference applications will expand at an 80 percent annual clip, underpinning guidance for sustained mid-50s gross margins and north of 25 percent year-over-year revenue growth in Q3.

Inference Leadership Poised To Accelerate Market Share Gains

Inference—the execution of trained models on new data—represents the lion’s share of AI compute demand moving forward. AMD CEO Lisa Su cites an 80 percent compound annual growth rate for this segment, and MI350 series adoption is on track to capture a disproportionate share of that expansion. Early deployments in high-throughput environments such as real-time language processing and recommendation systems have validated MI355’s TCO advantages, while pipeline deliveries to cloud and enterprise customers promise to shift share away from incumbents. As MI350 volumes ramp through the fall, AMD’s inference stack combines architectural leadership with an expanding software ecosystem, cementing its competitive position ahead of the next generational leap with MI400 Helios slated for 2026.

Valuation Upside Supported By Diversified Growth Catalysts

A dual-scenario discounted cash flow model yields a base-case target of $183 per share—implying 15 percent upside—and a bull-case valuation near $982 per share, reflecting up to 6× returns under sustained 80–100 percent revenue growth. Even under conservative assumptions—a 12.2 percent free cash flow margin, 5 percent terminal growth, and a 10 percent discount rate—AMD’s mid-cycle prospects for inference and client CPU leadership justify a premium multiple relative to peers. The combination of stable cost structure, expanding high-margin product mix, and emerging data-center share gains positions NASDAQ:AMD for outperformance as markets refocus on long-duration technology winners.

Tariff Exposure And Supply-Chain Resilience Underpin Risk Management

Prospective 100 percent U.S. tariffs on semiconductor imports create uncertainty, but AMD’s key foundry partner TSMC meets exemption criteria through its Arizona fabs and $165 billion domestic investment pledge. Packaging and testing suppliers ASE and Siliconware are actively evaluating U.S. expansion projects, while only Tongfu Microelectronics lacks a clear U.S. footprint and may face punitive levies. Management’s ability to retool procurement toward exempt partners ensures continuity of supply. Close monitoring of tariff legislation and strategic realignment of the partner network will mitigate downside, preserving gross-margin stability as AMD scales high-value inference deployments.

Insider Buying And China Trade Catalysts Signal Executive Conviction

COO Guido Philip’s $1 million share purchase in mid-May reflected deep management alignment with shareholder interests. The deliberate exclusion of China sales from Q3 guidance creates an embedded optionality: approval of MI308 and MI350 GPU export licenses could unlock a multi-hundred-million-dollar revenue stream in the coming quarters. As U.S.–China trade dialogues progress, the potential resumption of full product shipments stands as a high-conviction catalyst, augmenting a growth runway already fueled by sovereign AI initiatives and enterprise cluster rollouts.

Given the blend of Q2 durability, inference domain leadership, sovereign platform commitments, and robust cash-flow generation—coupled with manageable tariff risk and compelling insider signals—NASDAQ:AMD remains exceptionally well-positioned to capitalize on the next wave of AI spending.

That's TradingNEWS

Read More

-

Broadcom Stock Price Forecast: AVGO at $325 Ahead of AI-Driven Earnings

14.02.2026 · TradingNEWS ArchiveStocks

-

XRP Price Forecast: Ripple XRP-USD Climbs Back to $1.47 but $1.80 Wall and Sub-$1 Risk Still Dominate

14.02.2026 · TradingNEWS ArchiveCrypto

-

Natural Gas Futures Price Holds Around $3.20 as Storage Tightens and Winter Premium Fades

14.02.2026 · TradingNEWS ArchiveCommodities

-

Stock Market Weekly Recap: S&P 500 Stalls, Nasdaq Leads the Decline, Dow Eases as AMZN, NVDA, AAPL Sell Off

14.02.2026 · TradingNEWS ArchiveMarkets

-

GBP/USD Price Forecast - Pound Stuck at 1.36 as Fed Cut Hopes Clash With UK Weakness

14.02.2026 · TradingNEWS ArchiveForex